Pressure Pumping And Pricing Outlook

In our recent article, we have already discussed RPC’s (RES) Q4 2024 financial performance. Here is an outline of its outlook. In Q4, RES faced the typical seasonal slowdown, including operators’ budget exhaustion, holiday downtime, and adverse weather. Despite the general weakness in its other service lines, RES demonstrated relatively robust results in pumping as performance improved compared to Q3.

Pressure pumping generated higher revenues in Q4. Early 2025 indicators show that the spot market remains unchanged. The company estimates that the semi-dedicated market is supplied with sufficient horsepower capacity. Pricing, however, remains under pressure as OFS companies compete to maximize utilization.

RES’s management observes a “general optimism around the energy industry.” However, the energy supply and demand dynamics remain uncertain. The company would evaluate the policy and regulatory changes before providing any specific update. Any significant increase in energy supplies can pressure energy prices, adversely affecting completion activity.

Q4 Pressure Pumping Drivers

In Q4, RES opted to idle certain assets and operate only those assets that provide adequately high returns. Its Tier 4 DGB pumps and assets have better visibility with more dedicated customers. These assets have commitments through the majority of 2025. Its well-site performance with respect to gas substitution and efficiency has also been above par.

However, lower demand for legacy diesel equipment resulted in pricing undercuts. So, the company plans to upgrade its frac spreads. It will also assess the through-cycle economics before making any capital investments. When it invests in Tier 4 DGB assets, it will likely pull older equipment out of service to maintain the aggregate capacity.

Other Drivers

In Q4, RES’s coiled tubing business grew while revenues from the cementing operations also increased. However, downhole tools revenues declined due to seasonal factors. The company is optimistic about its recently introduced tools – a 3.5-inch downhole motor and lower pressure high-rate motor. It expects the momentum to continue in 2025.

RES does not plan on investing in electric fracs over a multiyear prospect. It is not currently competing in this segment. As the e-frac technology continues to evolve and change, it does not plan to compete in that from an organic perspective.

The Q4 Financial Results

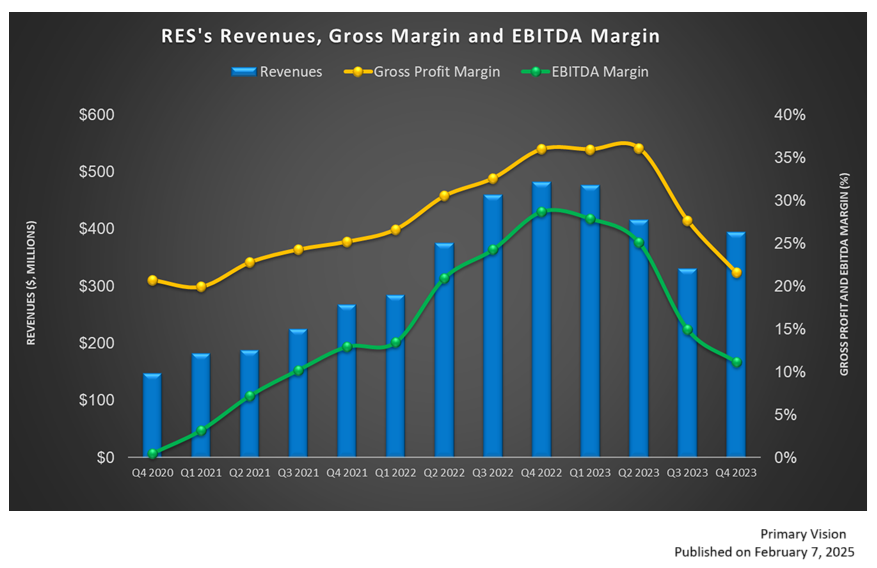

Quarter-over-quarter, RPC’s (RES) revenues decreased by 1% in Q4 due to lower customer activity. Revenues from pressure pumping operations increased while the sale of downhole and rental tools declined. Its adjusted EBITDA margin contracted by 270 basis points in Q4.

RES maintained a debt-free balance sheet as of December 31. Free cash flows, year-over-year, deteriorated in FY 2024 (39% down) because capex increased while cash flow from operations decreased. Over the past two years, its cumulative free cash flow exceeded $340 million.

Relative Valuation

RES is currently trading at an EV/EBITDA multiple of 4.6x. Based on sell-side analysts’ EBITDA estimates, the forward EV/EBITDA multiple is 4.5x. The current multiple is significantly lower than its five-year average EV/EBITDA multiple of 28.3x.

RES’s forward EV/EBITDA multiple is expected to contract versus its current EV/EBITDA multiple in contrast to a rise in the multiple for its peers. This implies that the company’s EBITDA is expected to decrease versus a rise in EBITDA for its peers in the next four quarters. This typically results in a lower EV/EBITDA multiple. The stock’s EV/EBITDA multiple is higher than its peers’ (PUMP, KLXE, and LBRT) average. So, the stock appears to be overvalued compared to its peers.

Final Commentary

At the end of Q4, RES produced a resilient pressure pumping result despite various challenges in the completion industry. Pricing remains under pressure as OFS companies compete to maximize utilization. Further increases in energy supplies can adversely affect the completion activity. However, the company’s Tier 4 DGBs are in high demand and have better visibility with more dedicated customers. So, it rebalanced its portfolio mix and upgraded its frac spread in the past year.

However, lower demand for legacy diesel equipment resulted in pricing undercuts. In other businesses, the company expects its recently introduced downhole motor and lower-pressure high-rate motor to perform well in 2025. RES maintained a debt-free balance sheet, although FCF declined significantly in FY2024. The stock is overvalued compared to its peers.

Premium/Monthly

————————————————————————————————————-