Natural gas prices have been climbing, and traders are betting that the rally isn’t over. With hedge funds holding their largest bullish position in U.S. gas markets since 2017 and global storage levels running low, the prospect of gas reaching $6/MMBtu is becoming more plausible. But if prices surge, what happens next? Will higher prices accelerate the push to capture and transport more gas to the Gulf Coast for LNG exports, or will pipeline constraints and infrastructure bottlenecks force producers to keep flaring? The balance between gas monetization, flaring reductions, and midstream capacity is shifting, and the industry is at a crossroads. If the market tightens further, the decision to either waste gas or commercialize it could shape the future of U.S. energy strategy in ways we haven’t seen before.

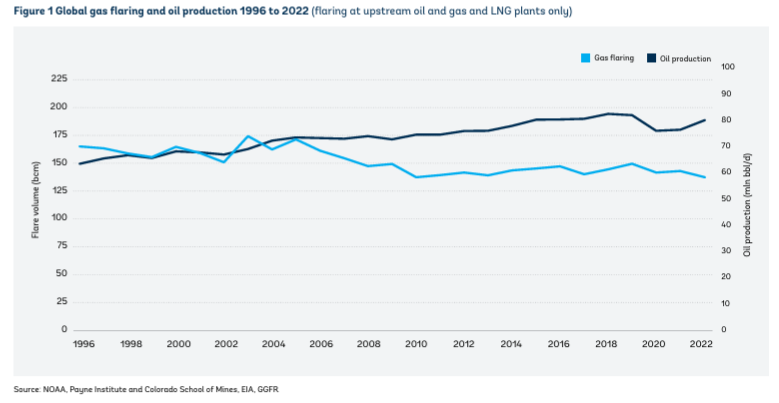

This article will integrate historical, regulatory, and market trends to explore whether rising natural gas prices could incentivize more gas to be transported to the coast rather than flared. The historical relationship between flaring and natural gas prices has shown that when prices were low, operators viewed associated gas as a nuisance rather than an asset, leading to widespread flaring. This was particularly evident in the Permian Basin in 2019 when pipeline constraints and sub-$1/MMBtu gas prices at the Waha Hub drove flaring to record highs. Conversely, when prices spiked above $5/MMBtu in 2021-2022 due to strong LNG demand and global supply disruptions, the economic incentive to capture gas increased, leading to a sharp reduction in flaring as operators prioritized gas infrastructure.

Regulatory shifts have also played a crucial role in reducing flaring. States like New Mexico have implemented stringent capture requirements, mandating that operators capture 98% of produced gas by 2026, while the EPA’s new methane rules are set to further limit flaring allowances. These regulations mean that even if gas prices remain low, operators are increasingly required to find solutions to monetize gas rather than burn it off. However, if prices were to rise toward $6/MMBtu, as hedge funds are currently betting on, the economic justification for capturing and transporting gas to coastal hubs would become even stronger.

Source: World Bank Global Gas Flaring Tracker

Current market trends suggest that the squeeze on global gas inventories and expectations for a tough summer refill season are pushing gas prices higher, reinforcing the case for capturing every available molecule. Hedge funds have built their largest bullish gas position since 2017, anticipating that falling production, rising exports, and increased power sector demand will keep prices elevated. This would make investments in gas processing and pipeline infrastructure more attractive, further reducing flaring rates.

Infrastructure capacity remains a critical factor. While new pipeline projects like the Matterhorn Express will help transport Permian gas to Gulf Coast markets, temporary constraints in early 2024 led to localized flaring spikes. This raises the question of whether additional midstream investments will be necessary if gas prices continue climbing. In the past, flaring has served as a release valve when infrastructure could not keep up with production growth. However, with LNG demand growing and policy pressures increasing, the incentive to expand gas capture and transport infrastructure is aligning with market forces.

If natural gas prices reach $6/MMBtu, it would likely accelerate this trend, prompting more gas to be directed to LNG terminals and industrial consumers rather than flared. The potential for new LNG contracts and higher returns on gas sales could further encourage operators to invest in gathering systems, compression facilities, and small-scale LNG solutions, particularly in areas where pipeline access remains limited. This price environment could also revive interest in mobile gas-powered generation units, allowing producers to monetize gas directly at the wellhead rather than waiting for takeaway capacity.

However, Mark Rossano, our senior analyst says that “we are already at the end of peak season and moving into shoulder season, We will see a lot of support to NG prices with spot cargoes flowing into Europe but we are passed the point that a spike to $6 would be possible.” However, “even in the absence of such a price incentive, flaring has been reduced down due to methane fee. A very important factor in this regard would be pipeline capacity – which is already tapped out.” We will discuss these issues in detail in our upcoming articles.

For now, the evolving landscape suggests that while flaring is already on a long-term decline due to regulation and infrastructure improvements, a sustained increase in natural gas prices could reinforce this trend by making gas capture even more economically compelling. The ability to send more gas to the coast would depend on the speed at which additional takeaway capacity can be built, but with global gas markets tightening, the motivation for such investments is growing. The coming months will reveal whether operators and midstream companies respond to higher prices with more aggressive gas capture and transport strategies or whether infrastructure bottlenecks continue to create short-term constraints.