Nabors plans to strengthen its international drilling activity in 2025 and 2026. Despite the recent rig suspensions, the SANAD JV continued to add newbuilds in Q4 and plans to see more additions in 2025. The company’s international rig margin will likely stay strong, while the US drilling margin can deteriorate in Q1.

Drilling Outlook

We have already discussed Nabors Industries’ (NBR) Q4 2024 financial performance in our recent article. Here is an outline of its strategies and outlook. The stability in international drilling allowed Nabors to activate 10 international rigs. A robust anticipated growth would prompt an additional nine rig start-ups and the reactivation of another rig in Colombia in 2025.

Incremental rig awards and redeployment of several rigs currently lying idle can flow through 2026 also. In the unconventional shale basins in Argentina, for example, it utilized idle rigs previously used in the U.S. In Kuwait, it will likely deploy a rig in Q1 2025, followed by two more in Q2. Other rig deployment opportunities lie in Asia, MENA (Middle East and North Africa), and Latin America.

SANAD Newbuilds

SANAD, NBR’s joint venture with Saudi Aramco, turned a corner after seeing a suspension in early Q4. SANAD deployed its ninth newbuild during Q4, while another five are scheduled for 2025. By 2026, it expects to have 15 working newbuilds. Saudi Arabia’s onshore natural gas activity will continue to expand. A similar prospect lies in the MENA market through 2025.

Investors may note that Saudi Arabia called for 50 rigs to be built over a 10-year period. NBR’s received a six-year initial term contract in this region. The early units generated more than $10 million in EBITDA per year, which can increase to $13 million with the recent deployments. The increase reflects cost inflation and a better rig mix. NBR’s management estimates that SANAD will recoup its investment within five years.

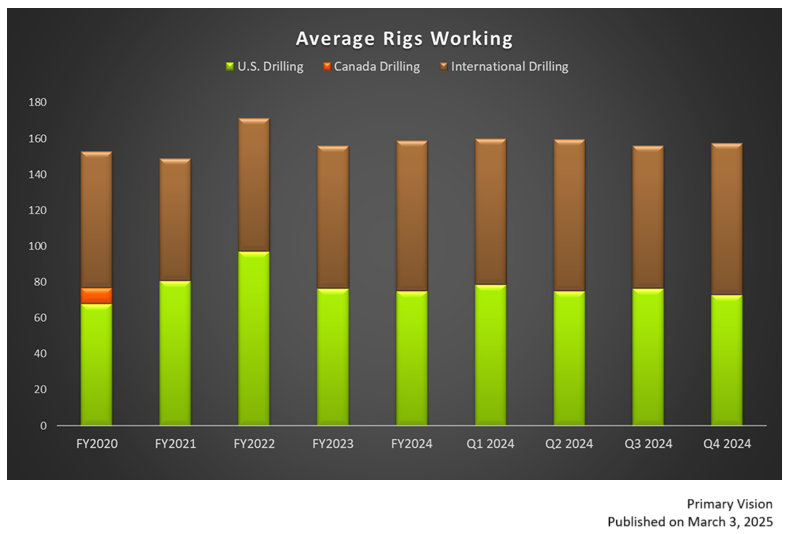

Industry & Rig Count Outlook

The industry rig count decreased by approximately 6% in the US onshore in the past year. However, NBR’s management believes that rig churn-outs can increase. Despite that, the leading-edge pricing for high-performance rigs is stable. In the US onshore, where NBR’s rig count dropped by 14% in FY2024 compared to FY2023, it can decrease further by 5-7 rigs in FY2025. In the US, the daily rig margin can decrease by 5% in FY2025. In international drilling, it is targeting an average daily margin of $17,600, or a rise of 6.8% compared to FY2024.

Margin Outlook

In Drilling Solutions, however, EBITDA decreased by 1.5% in Q4 versus Q3. Although managed pressure drilling contributed positively to EBITDA margin, deterioration in casing running more than offset the positives.

In NDS (Nabors Drilling Solutions), the gross margin expanded by 280 basis points in Q4. In Q1 2025, NBR expects the EBITDA margin in NDS to improve. Better penetration, higher revenue, and third-party rigs will likely offset the impact of lower US onshore activity.

In NDS and Rig Technologies, the total EBITDA grew in Q4 compared to Q3. The margin improvement resulted from the contribution from these capex-light segments. In Q4, contributions from these businesses increased to 19.5% of NBR’s consolidated EBITDA.

Financial Performance

Quarter-over-quarter, revenues in the company’s International Drilling operating segment witnessed a 1% rise in Q4, while the topline in the U.S. Drilling segment declined by 5%. In contrast, Rig Technologies witnessed a sequential revenue rise of 23%.

The company’s FCF turned negative in Q4. Its debt-to-equity (5.9x) is high, primarily due to low shareholders’ equity and a high long-term debt. In Q1 2025, it expects capex to decrease by ~17% compared to Q4. A large part of its Q1 capex will be spent on SANAD newbuilds.

Relative Valuation

NBR is currently trading at an EV/EBITDA multiple of 4.1x. Based on sell-side analysts’ EBITDA estimates, the forward EV/EBITDA multiple is lower. The current multiple is also lower than its five-year average EV/EBITDA multiple of 5.9x.

NBR’s forward EV/EBITDA multiple versus the current EV/EBITDA is expected to contract, contrasting the rise in multiple for its peers because the company’s EBITDA is expected to increase compared to a fall in EBITDA for its peers in the next four quarters. This typically results in a much higher EV/EBITDA multiple compared to its peers. The stock’s EV/EBITDA multiple is slightly higher than its peers’ (NINE, PUMP, and ACDC) average of 3.9x. So, the stock is reasonably valued, with a positive bias, compared to its peers.

Final Commentary

Buoyed by international drilling activity’s resilience, NBR reactivated many international rigs in 2024, to be followed by incremental startups in 2025 and 2026. Saudi Arabia, which saw rig suspensions in early Q4, recovered through plenty of newbuilds. Continued natural gas and unconventional shale activity, it plans to add more in 2025. Leading-edge pricing for high-performance rigs and rig margins remained stable in Q4. The margin improvement also resulted from the capex-light NDS and Rig Technologies.

The US onshore rig count was relatively shaky in Q4. In this region, the rig count and daily rig margin can drop further in Q1 2025. The company’s FCF turned negative in FY2024. It aims to improve FCF by reducing capex in FY2025. The stock is reasonably valued, with a positive bias, compared to its peers.

Premium/Monthly

————————————————————————————————————-