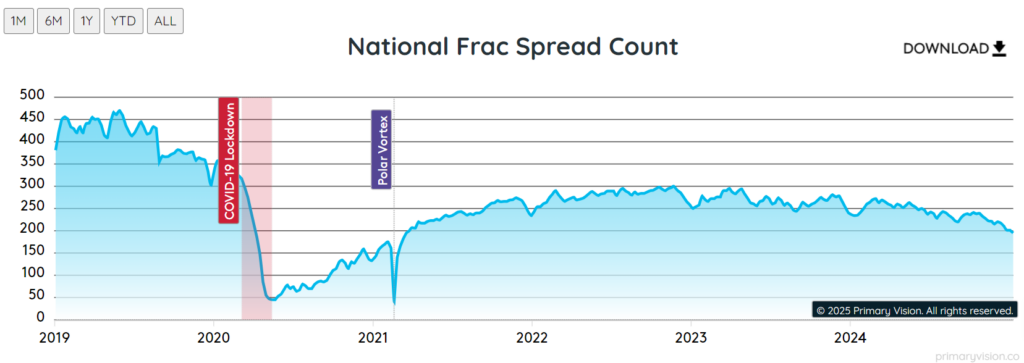

The Frac Spread Count (FSC) serves as a critical barometer for U.S. shale activity, providing insights into the pulse of the fracking industry. By tracking the number of active frac spreads—units essential for hydraulic fracturing operations—the FSC offers a real-time measure of operator activity and capital deployment across key shale basins. Its significance extends far beyond operational metrics, as it directly correlates with broader trends in oil and natural gas markets. A rising FSC often signals increased confidence among operators, driven by favorable oil prices and demand outlooks, while a declining FSC reflects caution, cost-cutting, or subdued market conditions. As short-cycle production in U.S. shale responds quickly to price volatility, the FSC becomes a leading indicator of supply dynamics, influencing everything from rig count forecasts to investment decisions. Understanding FSC trends allows stakeholders to connect the dots between market sentiment, price shifts, and the future trajectory of the energy sector.

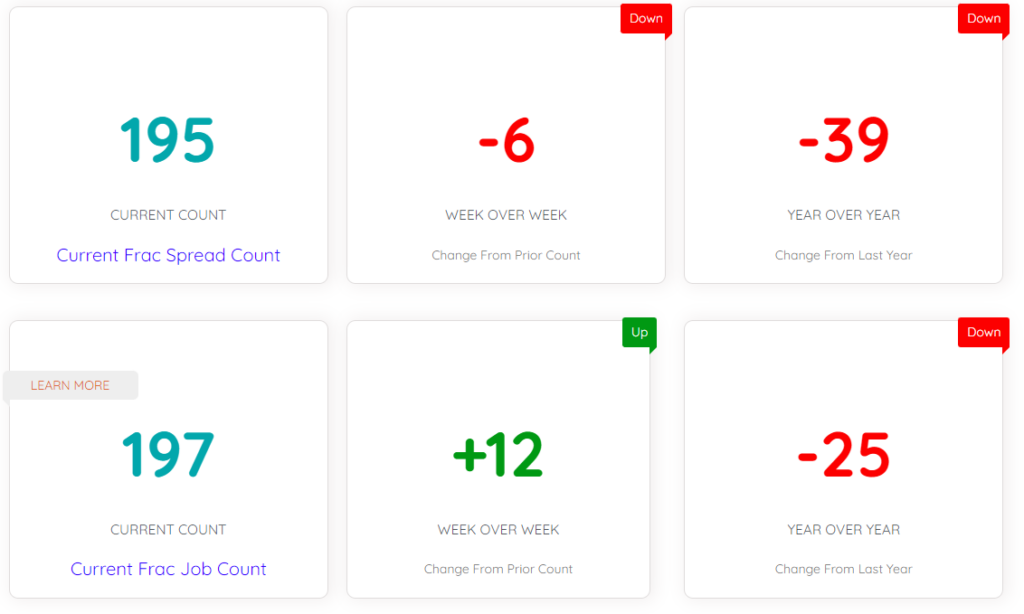

The recent decline in the U.S. Frac Spread Count (FSC) highlights evolving dynamics in the oilfield services sector. With the current FSC at 195, reflecting a 6-unit week-over-week drop and a 39-unit year-over-year decline, the U.S. fracking landscape is visibly under pressure. While the Frac Job Count showed a minor weekly increase to 197, the annual drop of 25 jobs points to broader challenges impacting the sector. These trends reflect reduced operator activity, cautious spending, and potential overcapacity in certain markets.

This downturn in spreads iis happening when the wider picture in the oil markets is consistently evolving. We are expecting a continued slowdown in U.S. oil production growth. Other estimates show that liquids growth is forecasted to fall to just 367 kb/d in 2025, down from 734 kb/d in 2024. The cautious production outlook aligns with the declining FSC, as lower operator activity translates directly to fewer deployed frac spreads. A closer look at the FSC reveals not just cyclical headwinds but also structural shifts in the industry. Operators are increasingly focused on capital discipline and longer-term projects, prioritizing efficiency over rapid expansions.

The connection between oil prices and fracking activity is also apparent. The projected dip in crude prices to lower-$60 levels could further squeeze short-cycle production, which U.S. shale is heavily reliant on. Historically, every $10-per-barrel drop in oil prices reduces short-cycle capital expenditures by 5-10%, impacting frac activity directly. While long-cycle resources like offshore projects remain more insulated, the short-term market volatility adds layers of complexity for service providers.

Companies are making adjustments. Take for instance, Halliburton that is using innovation and operational resilience to overcome such problems. In its Completion business, 90% of its fracturing spreads are already committed for work in 2025, driven by advanced technologies such as the Zeus platform, electric pumping units, and the Octiv AutoFrac solution. Octiv automates key stages of frac jobs, from ramp-up to ramp-down, significantly improving efficiency on multi-well pads. During Q3, Halliburton secured contracts for two additional e-frac spreads and extended several existing fleet agreements. This integration of automation, real-time diagnostics, and sustainability underscores companies’ focus on higher efficiency and improved recovery rates. Meanwhile, SLB continues to focus on international resilience and technology diversification. STEP energy services is anticipating a “worse-than-usual Q4 because of the weakness of energy prices” as pointed by our analyst Avik Chowdhury in another article for Primary Vision.

The current FSC figures reflect these operational adjustments and hint at future consolidation, with smaller service providers struggling to maintain competitiveness.

Natural gas markets provide a partial counterbalance to this narrative. Bullish trends in U.S. and European gas demand, driven by colder-than-normal weather, have supported prices and led to inventory draws. While this may not directly influence FSC, the broader energy market recovery could provide some support for fracking activity if oil and gas prices stabilize or increase. Looking ahead, the decline in FSC serves as a leading indicator of restrained operator activity and cautious spending. However, it also signals opportunities for efficiency gains and technological adoption in the sector. As service providers navigate these challenges, the industry’s ability to balance cost discipline with operational readiness will determine the trajectory of active frac spreads in the coming year.