The question of where U.S. oil production growth will originate in 2025 is no longer as simple as adding more rigs and frac spreads. While the Energy Information Administration (EIA) has raised its forecast for U.S. crude production to 13.59 million barrels per day (bpd), Primary Vision’s latest frac spread count (FSC) and frac job count (FJC) data indicate that growth will not be evenly distributed across all basins. Instead, it will be highly concentrated in specific regions, driven by operators that can maximize productivity with fewer resources. This article will break down the frac supply landscape, analyze which regions have the greatest potential for growth, and assess whether the available hydraulic horsepower (HHP) is enough to support rising production levels.

The State of Frac Activity: Where Are the Active Spreads?

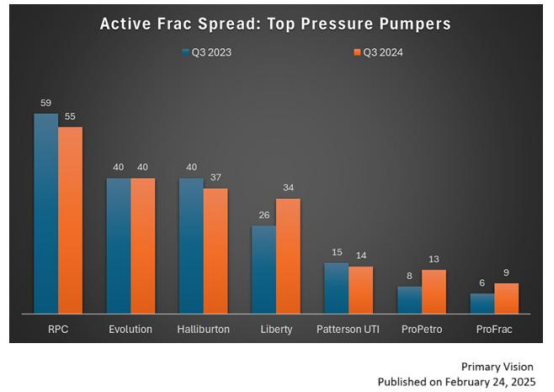

Primary Vision’s data showcase that the Permian dominates the frac spread landscape, accounting for 129 spreads and 7.16 million active hydraulic horsepower (HHP)—more than half of total frac’ing activity. The Appalachian Basin (Marcellus & Utica) and the Western Gulf (Eagle Ford) follow at a distant second and third with 25 and 23 active spreads, respectively. Meanwhile, regions like the Williston (Bakken) and Anadarko play a much smaller role.

This distribution underscores a key trend: the Permian remains the primary driver of U.S. production growth, while other basins exhibit stagnation or limited upside. The activity disparity suggests that operators are prioritizing capital allocation toward regions with the highest breakeven advantages and infrastructure accessibility. However, despite the Permian’s leadership, the activity has not returned to pre-2020 completion activity levels, as corporate strategies continue to prioritize capital returns over production expansion.

The Untapped Potential: How Much HHP Is Sitting Idle?

The underutilization of marketed HHP presents another critical dynamic. While the U.S. has 16.5 million marketed HHP, only 13 million is currently active, leaving 21.1% of total HHP capacity idle. This suggests that additional capacity exists to ramp up activity if price incentives align, but capital discipline and supply chain constraints remain key obstacles.

If we break this down further, the largest portion of idle capacity exists in basins with fewer active spreads. For example, the Anadarko Basin hosts only 7 active spreads despite historically being a key production region, while the Williston, with only 17 active spreads, holds significantly more idle HHP than currently deployed. This raises an important question: what would it take to bring some of this capacity online?

Historically, operators would quickly reactivate idle equipment when oil prices rose. However, this time around, labor shortages, rising service costs, and strict capital budgets are keeping a lid on activity expansion. Unless we see a structural shift in oil prices or a relaxation in capital discipline, much of this idle HHP is likely to remain offline—meaning that U.S. production growth will have to come from existing active fleets through further efficiency improvements rather than a major expansion in frac activity.

Who Will Lead the Growth?

So, the big question is: Where will new production come from if overall completion activity remains below previous peaks? The answer lies in longer laterals, high-intensity completions, and strategic capital deployment. A single frac spread today can complete significantly more lateral footage per month than it could in 2019. Apart from this, the rise in frac efficiency is also about technological advancements that allow operators to do more with less. For instance, 18% of active spreads are now electric-powered rather than diesel, dramatically reducing fuel costs and emissions.

This means production growth can continue with fewer spreads, provided operators concentrate in high-return areas like the Delaware Basin within the Permian.

Looking beyond just frac spreads, company announcements provide another layer of insight. ExxonMobil, Chevron, and Pioneer Natural Resources have signaled continued investment in the Permian, albeit with a focus on efficiency over sheer volume expansion.

- ExxonMobil’s Permian production grew 12% year-over-year in 2024, and the company has hinted at further optimization-driven growth in 2025. Exxon’s focus remains on high-efficiency drilling, leveraging longer laterals and tighter completion designs to extract more from each well rather than dramatically increasing well count.

- Chevron, on the other hand, has taken a more cautious approach, emphasizing cash returns. However, it still views the Permian as a cornerstone of its long-term strategy, meaning that even if its spending remains controlled, its production gains could still be material.

- Pioneer’s integration with Exxon could unlock synergies that drive further development. With Exxon’s economies of scale, Pioneer’s acreage in the Midland Basin could see increased activity without dramatically increasing overall frac spread deployment.

What About Other Basins?

Outside the Permian, growth potential is more uncertain. The Appalachian Basin, while maintaining 25 active spreads, is heavily dependent on natural gas prices, which remain soft due to high storage levels and limited LNG export capacity. However, this might change as we have scene inventory drops across Europe. Still , without a strong price signal, any meaningful expansion in completions here seems unlikely in the near term.

Source: John Kemp Chartbook

The Bakken (Williston Basin) and Eagle Ford are also seeing limited expansion, with operators focusing more on cash flow than aggressive drilling. While some independents may reactivate additional spreads if oil prices strengthen, neither region is positioned for major production growth relative to the Permian.

Will Tariffs and Trade Tensions Play a Role?

One wildcard in this equation is the impact of tariffs on North American crude flows. A potential 25% tariff on Mexican crude could disrupt supply chains, leading refiners to seek alternative feedstocks, possibly increasing demand for U.S. light sweet crude. However, this assumes that U.S. shale producers can ramp up output quickly to fill the gap. If costs remain high and budgets constrained, any production response could be muted. This would mean that refiners might instead turn to Middle Eastern and Latin American barrels, reducing the expected impact on U.S. shale activity.

In summary, U.S. production growth in 2025 will largely come from the Permian, with incremental contributions from other basins where efficiencies can be maximized. The industry’s ability to convert idle HHP into active completions will depend on price signals, cost structures, and corporate strategies. If oil prices remain in the $70-$75 range, we are unlikely to see a dramatic reactivation of inactive spreads. Instead, operators will lean on efficiency gains to drive incremental production growth. If, however, prices rise above $85, we could see some of the 3.48 million idle HHP return to service, pushing more completion activity into the Williston, Anadarko, and Appalachian Basins.

For now, the Permian remains the dominant growth engine, and Primary Vision’s FSC and FJC data will be crucial in tracking these trends in real time—helping our readers anticipate where the next wave of U.S. oil supply will originate.